It is a financial instrument, issued by Companies to raise Funds from the Market that acknowledges Payment of Interest on regular intervals and Repayment of Principle on maturity of the instrument to its holders.

It includes Debentures, Stock, Bonds or any other Instrument of a Company that evidences debt on it.

It can be redeemable (having maturity period) or Irredeemable (No maturity period.) (Explanation of Types of Debentures has been ignored intentionally.)

Disclosure of Debentures in Balance Sheet

Debenture is generally a long term Financial Instrument, a means of raising Long term Finance for the Company that falls under Non Current Liability Head in Balance Sheet.

An Extract of Balance Sheet

| Equity & Liability: Non Current Liability: Long Term Borrowings Current Asset: Cash & Cash Equivalent | Note No. 1 2 | Amount |

| Notes to Accounts: 1. Long Term Borrowings (…….. ….% Debentures of Rs … each) 2. Cash & Cash Equivalent: Cash in Hand or Bank | Amount |

However, if it has been issued for a period of Less than 12 Months, then it falls under Short Term Borrowing under Current Liability Head of Balance Sheet.

| Equity & Liability: Current Liability: Short Term Borrowings Current Asset: Cash & Cash Equivalent | Note No. 1 2 | Amount |

Note:

In Case, Part of Long Term Debentures become due for redemption before maturity within 12 months from the date of Balance Sheet, it will be recorded in Other Current Liability under Current Liability Head as “Current Maturities of Long Term Debts”.

Issue of Debentures

Debentures can be issued for Cash or Consideration other than Cash.

Further, whether issued in Cash or For Consideration other than Cash, it can be issued at Par, Premium or Discount.

Issue of Debentures for Cash

Two methods

Debentures Payable in Lump sum

It means when payment of Debentures is received in one instilment.

Debentures Payable in Installments:

Payment of Debentures is received in installments.

First installment comes with application known as application money, Second- allotment, third -First call, fourth – Second call and so on. Last installment is also called as Final call.

Accounting Entries for issue of Debentures Payable in Lump sum

Issued at Par

1. On receipt of Application money

Bank A/c ……………………….Dr

To Debenture Application A/c

2. On Allotment of Debentures

Debenture Application A/c……….Dr

To Debenture A/c

3. On refund of Excess Application Money:

Debenture Application A/C………..Dr

To Bank A/C

Note: We can also write Debenture Application & Allotment A/C instead of Debenture Application A/C.

Accounting Entries for issue of Debentures Payable in Lump sum

1. On receipt of Application money

Bank A/c ……………………….Dr (Total Application money including Premium)

To Debenture Application A/c

2. On Allotment of Debentures

Debenture Application A/c……….Dr (Total Application money including Premium)

To Debenture A/c (with Nominal/ Face value)

To Security Premium Reserve A/c (with Premium amount)

Accounting Entries for issue of Debentures Payable in Lump sum

1. On receipt of Application money

Bank A/c ……………………….Dr (Total Application money)

To Debenture Application A/c

2. On Allotment of Debentures

Debenture Application A/c……….Dr (Total Application money received)

Discount on Issue of Debentures…….Dr (Total Discount Allowed)

To Debenture A/c (with Nominal/ Face value)

Accounting Entries for issue of Debentures Payable in Installments

Issued at Par

1. On receipt of Application money

Bank A/c ……………………….Dr

To Debenture Application A/c

2. on Allotment of Debentures

Debenture Application A/c……….Dr

To Debenture A/c (with nominal/ face value)

3. Amount due on allotment

Debenture allotment A/c……..Dr

To Debenture A/c

4. On receipt of allotment money

Bank A/c………………………Dr

To Debenture Allotment A/c

5. On First call being Due

First Call A/c…………….Dr

To Debenture A/c

6. On receipt of First Call

Bank A/c ……………….Dr

To First Call A/c

7. On Second & Final Call being Due

Second & Final Call A/c……….Dr

To Debenture A/c

8. On receipt of Second & Final Call

Bank A/c ……………..Dr

To Second & Final Call A/c

Accounting Entries for issue of Debentures Payable in Installments

Issued at Premium:

Case I. When premium is received at the time of application along with application money:

1. On receipt of Application money

Bank A/c ……………………….Dr (Total Application money including Premium)

To Debenture Application A/c

2. on Allotment of Debentures

Debenture Application A/c……….Dr (Total Application money including Premium)

To Debenture Capital A/c (with nominal/ face value)

To Security Premium Reserve A/c (with Premium amount)

Note:

All other Entries for allotment, First call and final call will remain similar as to the case of Debentures issued at Par.

Case II. When premium is receivable at the time of Allotment:

1. On receipt of Application money

Bank A/c ……………………….Dr

To Debenture Application A/c

2. on Allotment of Debentures

Debenture Application A/c……….Dr

To Debenture Capital A/c (with nominal/ face value)

3. Amount due on Allotment including Security Premium

Debenture allotment A/c……..Dr

To Debenture Capital A/c

To Security Premium Reserve A/c

4. On receipt of allotment money including Security Premium

Bank A/c………………………Dr

To Debenture Allotment A/c

Note:

If question is silent with regard to receipt of Security Premium, it is assumed that it is due with allotment money.

All other Entries for First call and final call will remain similar as to the case of Debentures issued at Par.

Case III. When premium is receivable at the time of Application, Allotment and all Calls:

1. On receipt of application money

Bank A/c ……………………….Dr (Total Application money including Premium)

To Debenture Application A/c

2. on allotment of Debentures

Debenture Application A/c……….Dr (Total Application money including Premium)

To Debenture Capital A/c (with nominal/ face value)

To Security Premium Reserve A/c (with Premium amount)

3. Amount due on allotment including Security Premium

Debenture allotment A/c……..Dr

To Debenture Capital A/c

To Security Premium Reserve A/c

4. On receipt of allotment money including Security Premium

Bank A/c………………………Dr

To Debenture Allotment A/c

5. On First call being Due including Security Premium

First Call A/c…………….Dr

To Debenture Capital A/c

To Security Premium Reserve A/c

6. On receipt of First Call including Security Premium

Bank A/c ……………….Dr

To First Call A/c

7. On Second & Final Call being Due including Security Premium

Second & Final Call A/c……….Dr

To Debenture Capital A/c

To Security Premium Reserve A/c

8. On receipt of Second & Final Call including Security Premium

Bank A/c ……………..Dr

To Second & Final Call A/c

Accounting Entries for issue of Debentures Payable in Installments

1. On receipt of Application money

Bank A/c ……………………….Dr

To Debenture Application A/c

2. on Allotment of Debentures

Debenture Application A/c……….Dr

To Debenture A/c (with nominal/ face value)

3. Amount due on allotment

Debenture allotment A/c……..Dr

Discount on Issue of Debentures A/C ……Dr

To Debenture A/c

Note: Until and unless specified in the question; The amount demanded on Allotment is assumed to be net of Discount.

4. On receipt of allotment money

Bank A/c………………………Dr

To Debenture Allotment A/c

5. On First call being Due

First Call A/c…………….Dr

To Debenture A/c

6. On receipt of First Call

Bank A/c ……………….Dr

To First Call A/c

7. On Second & Final Call being Due

Second & Final Call A/c……….Dr

To Debenture A/c

8. On receipt of Second & Final Call

Bank A/c ……………..Dr

To Second & Final Call A/c

Accounting Treatment & Disclosures in relation to Discount or Loss on Issue of Debentures

Discount or Loss on Issue of Debentures is a capital loss which can be written off against

1. Security Premium Reserve or

2. Profit & Loss A/C

A Company can write off Discount or Loss on Issue of Debentures in two ways:

1. In first Year itself either from Security Premium Reserve A/C or P&L A/C.

2. Writing Off amount of Discount or Loss on Issue of Debentures in equal Installments every year over the maturity period of Debentures.

For Example

Company issues 1000 Debentures of Rs. 100 at 10 % Discount and to be redeemable after 5 years at 20 % Premium. Loss on issue is to written off in 5 equal installments over 5 Years maturity period.

Amount to be written Off every Year = Rs. 3000 ÷ 5 = Rs.600

Journal Entry for writing off Loss on Issue of Debentures:

P&L A/C or Security Premium Reserve A/C …..Dr

To Discount or Loss on Issue of Debentures

Disclosure of Unamortised Discount on Issue of Debentures to be written off within 12 months:

It is shown under the Head ‘Current Asset’ & Sub Head ‘Other Current Asset’ in Balance Sheet.

Disclosure of Remaining Balance of Unamortised (Not Written off) Discount on Issue of Debentures :

It is shown under the Head ‘Non Current Asset’ and Sub Head Other ‘Non Current Asset’.

For Example:

500 Debentures of Rs. 100 each at a discount of Rs. 20 on 1 April 2017. Discount on Issue will be written off in 4 Equal Installments then in this case Total Discount is = Rs. 20 × 500 =Rs. 10000.

Discount to be written off every year = Rs. 10000 ÷ 4 = Rs. 2500

Discount to be written off during April 1, 2017 – 31 March 2018 = Rs. 2500.(This amount will be written off this year, So No entry for this amount in Balance Sheet.)

Discount to be written off in next Operating cycle that is within 12 months from the date of Balance Sheet = Rs. 2500.

Amount to be written off after 12 months= Rs. 10000 – Rs. 2500 – Rs. 2500 = Rs. 5000.

Disclosure in Balance Sheet of Above Data will be:

Non Current Asset:

Other Current Assets 5000

Current Asset: Other Current Assets 2500

Issue of Debentures for Consideration Other than Cash

Issue of Debentures to Vendors for Purchase of Fixed Asset or Business

On Purchase of Assets:

Sundry Asset A/C……Dr

To Vendor’s A/C

On Purchase of Business:

Sundry Assets A/C……………Dr (Agreed Value of Assets)

Goodwill A/C …………………Dr*

To Sundry liabilities A/C (Agreed Value of Liabilities)

To Vendor A/C (With Purchase Consideration)

To Capital Reserve A/C**

*If Purchase Consideration > Net Asset Value, then difference is debited to Goodwill A/C.

**If Purchase Consideration < Net Asset Value, then difference is credited to Capital Reserve A/C.

Either Goodwill A/C or Capital Reserve A/C will be written at a time. Both cannot come together.

Calculation of Number of Debentures to be issued = Purchase Consideration ÷ Issue Price of One Debenture

On Issue of Debentures at Par

Vendor A/C……………………Dr (With Purchase Price)

To Debenture Cap A/C (With Nominal or Face Value of Debentures)

Issue Price = Par value of Debenture

On Issue of Debentures at Premium

Vendor A/C……………………Dr (With Purchase Price)

To Debenture Cap A/C (With Nominal or Face Value of Debentures)

To Security Premium Reserve A/C (if Debentures have been issued at Premium)

Issue Price = Par value of Debenture + Security Premium Reserve

On Issue of Debentures at Discount

Vendor A/C……………………Dr (With Purchase Price)

Discount on Issue of Debenture A/C …Dr (If issued at Discount)

To Debenture Cap A/C (With Nominal or Face Value of Debentures)

Issue Price = Par value of Debenture – Discount on Issue of Debenture

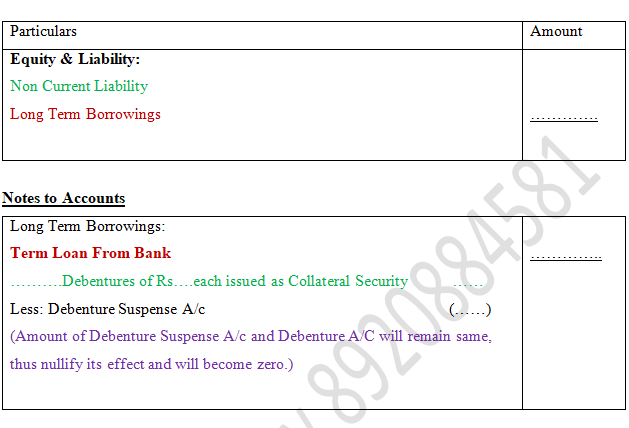

Issue of Debentures as Collateral Security:

It means issue of Debentures as an additional security or Collateral against the Loan in addition to the principal or main security.

Two Methods for Accounting Issue of Debentures as Collateral Security:

Method 1. No Journal Entry is passed for issue of Debentures. It is disclosed by way of information written in bracket with Long Term Borrowings under Non Current Liability or Short Term Borrowings under Current Liability.

Case I: Disclosure of Debentures issued as Collateral Security under Long Term Borrowings in Non Current Liability Head.

Extract of Balance Sheet

Method 2: When Debentures issued as Collateral Security are recorded in the Books of Account:

Debenture Suspense A/C is created against Debentures issued.

Journal Entry passed in this case will be:

Debenture Suspense A/C…….Dr

To Debenture A/C

When Loan is repaid to the lender, we reverse the above entry.

Disclosure in Balance Sheet

Case I: Disclosure of Debentures issued as Collateral Security under Long Term Borrowings in Non Current Liability Head.

Extract of Balance Sheet

Rights of Lender in case of Non Payment of Loan:

Lenders can recover the Loan amount by selling Debentures or by redemption of Debentures:

No Journal entry is passed if lender does not exercise rights as no immediate Liability is by issuing Debentures as Collateral Security.

Journal Entries passed in case Lender exercise his/ her rights:

For reversing the entry for issue of Debentures as Collateral Security

Debenture A/C……….Dr

To Debenture Suspense A/C

For Conversion of Debentures issued as Collateral security into Liability along with interest Due on it:

Loan A/C………………….Dr (with Principal Amount)

Outstanding Interest A/C …….Dr

To Debentures A/C (Principal + Outstanding Interest)

Various Cases related to Redemption of Debentures:

Debentures issued either at Par, Premium or Discount can be redeemed at Par or Premium.

Case I: Debentures issued at Par, Redeemable at Par

On Receipt of Application Money

Bank A/C……….Dr

To Debenture Application A/C

On Transfer of Application Money to Debenture A/C

Debenture Application A/C………Dr

To Debenture Allotment A/C

Case II: Debentures issued at Discount, Redeemable at Par

On Receipt of Application Money

Bank A/C……….Dr

To Debenture Application A/C

On Transfer of Application Money to Debenture A/C & Recording of Discount on Issue

Debenture Application A/C………Dr

Discount on Issue of debenture A/c…..Dr

To Debenture Allotment A/C

Case III: Debentures issued at Premium, Redeemable at Par

On Receipt of Application Money

Bank A/C……….Dr

To Debenture Application A/C

On Transfer of Application Money to Debenture A/C & Recording of Premium on Issue

Debenture Application A/C………Dr

To Debenture Allotment A/C

To Security Premium Reserve A/C

Note:

No Extra entries have been passed as amount payable at the time of Redemption is Equal to Nominal Value.

Case IV: Debentures issued at Par, Redeemable at Premium

Company will suffer a loss equal to Premium amount payable at the time of redemption. So it is debited to Loss on Issue of Debentures A/C at the time of allotment following principle of Prudence of Recording anticipated losses to companies in future.

On Receipt of Application Money

Bank A/C……….Dr

To Debenture Application A/C

On Transfer of Application Money to Debenture A/C

Debenture Application A/C………Dr

Loss on Issue of Debenture A/C…..Dr

To Debenture Allotment A/C

To Premium on Redemption of Debenture A/C

Case V: Debentures issued at Discount, Redeemable at Premium

In this case, Company will suffer a loss equal to Premium amount payable at the time of redemption as well as loss incurred due to Discount offered at the time of issue.. Both these losses are debited to Loss on Issue of Debentures A/C at the time of allotment following principle of Prudence of Recording anticipated losses to companies in future.

On Receipt of Application Money

Bank A/C……….Dr

To Debenture Application A/C

On Transfer of Application Money to Debenture A/C

Debenture Application A/C………Dr

Loss on Issue of Debenture A/C…..Dr (with Discount on issue+ Premium on Redemption)

To Debenture Allotment A/C

To Premium on Redemption of Debenture A/C

Or

We can also write both losses separately that is:

On Transfer of Application Money to Debenture A/C

Debenture Application A/C………Dr

Loss on Issue of Debenture A/C…..Dr (Premium on Redemption)

Discount on Issue of Debenture A/C….Dr (Discount on Issue)

To Debenture Allotment A/C

To Premium on Redemption of Debenture A/C

Case V: Debentures issued at Premium, Redeemable at Premium

In this case, Company will suffer a loss equal to Premium amount payable at the time of redemption and a Capital receipt at the time of issue of Debentures in the form of Security Premium. Loss is to be debited to Loss on Issue of Debentures A/C at the time of allotment following principle of Prudence of Recording anticipated losses to companies in future and Security Premium received will be credited.

On Receipt of Application Money

Bank A/C……….Dr

To Debenture Application A/C

On Transfer of Application Money to Debenture A/C

Debenture Application A/C………Dr

Loss on Issue of Debenture A/C…..Dr (with Premium on Redemption)

To Debenture Allotment A/C

To Premium on Redemption of Debenture A/C

To Security Premium Reserve A/C

Note:

Loss on Issue of Debentures is a Capital Loss and it can be written off either from Security Premium Reserve A/C or P&L A/C with in maturity period of Debentures. Generally these losses are distributed equally over maturity period of Debentures. However it can be written off at one time also.

Accounting treatment for amortization or writing off of Loss on Issue of Debenture is similar to Discount on issue of Debentures as discusses earlier in the column of Accounting Treatment & Disclosures in relation to Discount or Loss on Issue of Debentures.

Premium on Redemption of Debenture is a liability for the company. It is shown under Other Long Term Liabilities in Non Current Liability Head, when Debentures are shown as Long Term Borrowings under Non Current Liability Head.

However, when Debentures are shown as Current Maturities of Long Term Debt, Premium on Redemption of Debenture is also shown under the head Current Liability & Sub Head Other Current Liability.

Interest on Debenture is calculated on Nominal / Face value, whether it has been issued at Par, Premium or Discount.

Interest rate also means coupon rate, which is mentioned with Debenture.

For example In 12 % Debenture of Rs. 100 each; Interest or Coupon rate is 12% and Interest will be calculated on Face value that is 12 %of Rs. 100 = Rs. 12.

Interest on Debenture is a charge against profit.

Interest Payment may be subject to Tax Deducted at source (TDS) which is always calculated on Interest amount.

For example, if TDS is 10 %, then from the above example TDS chargeable will be 10 % of Rs. 12 = Rs. 1.2.

Journal Entries related to Interest on Debenture & TDS:

When Interest is due and TDS is applicable:

Debenture Interest A/C….Dr

To Debentureholders’ A/C

To TDS Payable A/C (No entry of TDS Payable if question does not ask for TDS)

When Interest is Paid:

Debentureholders’ A/C…..Dr

TDS Payable A/C………….Dr (No entry of TDS Payable if question does not ask for TDS)

To Bank A/C

For Transfer of Interest at the end of the year to P& L A/C as an expense (Finance Cost)

P&L A/C………..Dr

To Interest on debenture A/C

3 Comments

gate io telegram · May 20, 2023 at 4:08 pm

I am a website designer. Recently, I am designing a website template about gate.io. The boss’s requirements are very strange, which makes me very difficult. I have consulted many websites, and later I discovered your blog, which is the style I hope to need. thank you very much. Would you allow me to use your blog style as a reference? thank you!

Increasing Demand of Home Tutors & Home tuitions in Noida – RBL Academy · March 7, 2023 at 10:40 pm

[…] Class 11 home tuition & class 12 home tuition in Noida […]

Benefits of Hiring a Home Tutor for Class 11 and 12 Accounts and Economics – RBL Academy · March 28, 2023 at 9:52 pm

[…] you with mock tests, previous years’ question papers, and tips on time management. The tutor will also focus on strengthening your weak areas and improving your overall […]