AS- 3 Cash Flow Statement notes, CFS format, Cash Flow from Operating, Financing & Investing Activity, Change in Working Capital, Cash & Cash equivalent & CFS Specimen

AS- 3 Cash Flow Statement

- A statement that shows flow of cash and cash equivalents of a particular period of time. It is a summary of receipts and payment of cash for a particular period of time. It also explains reasons for the changes in cash position of the firm.

- Cash flow statement is generally prepared for one financial year (April to March).

- Cash means cash in hand and cash at bank /demand deposits with banks.

- Cash equivalent is a highly liquid investment whose maturity period is three months or less. It is subject to a minimal risk of a change in value.

- Cash equivalent includes Marketable securities / short term investment, short term deposits in banks, cheques and drafts on hand, certificate of deposits.

Note – Until and unless, question specifies, short term investment is considered as marketable securities. Otherwise it will be taken as current asset while solving question.

- Cash Flow means inflow and outflow of cash and cash equivalents.

- Inflow – Any transaction that increases cash and cash equivalent of a company

Example –rent received cash revenue from operations, sale of investment etc.

- Outflow – any transaction that decrease inflow and outflow of a company.

Example – repayment of loans and advances, payment to creditors, operating expenses paid etc.

AS -3 requires preparation of cash flow statement under three heads:

It includes cash flows from the principal revenue generation activities of an organisation.

It includes cash flows from sale and purchase of noncurrent assets, investments (which are not included in cash equivalent) and earning generated on those investments.

It includes cash flow resulting out of change in shareholders’ fund and noncurrent liability of an organisation (raising and repaying finance of an organisation).Note – We will see the examples of all three activities in CFS format.*

| Cash Flow Statement (As per revised AS 3) For the year ended……….. | Rs. | Rs. | |

| Net Profit as per Profit and Loss A/c (C.Y. – P.Y.) (given in notes to accounts) Add: Transfer to general reserve (C.Y. – P.Y.) Proposed dividend (p.Y.) Interim dividend/ final dividend paid during the year (Given in additional information) Provision for tax (C.Y., if no additional information regarding tax is given in the question) Any other provisions* Any expenses written off* Extraordinary items, if any, debited to P &L A/c Less : Extraordinary Items, if any, credited to P & L A/c Refund of Tax credited to Profit and Loss A/c | |||

| A. Net profit before taxation and Extra ordinary items Adjustment for Non-Cash and Non-Operating Items Add : Depreciation Discount on issue of shares and debentures written off Interest paid on long term & short term borrowings, debentures, bank overdraft /cash credit Loss on sale of fixed assets and investment Patent, copyright, trademark, goodwill and other non tangible assets written off (P.Y. – C.Y.) Preliminary expenses written off (P.Y. – C.Y.) Premium paid on redemption of Preference shares / debentures Less : Interest received Dividend income received Rental income received Profit/ gain on sale of fixed asset & Investment | |||

| B. Operating profits before working capital changes Add: Decrease in current assets and increase in current liabilities Less : Increase in current assets and decrease in current liabilities | |||

| C. Cash generated from operations Less : Net Income tax paid (Income tax paid – tax refund) | |||

| D. Cash flow before extraordinary items (+/-)Adjusted extraordinary items (eg. subtract compensation paid on voluntary retirement scheme) | |||

| I. Cash flow from Operating Activity / Cash used in operating activity | |||

| Cash Flow from investing Activity Add : Sale of fixed assets Sale of non-current investments Sale of intangible assets such as goodwill, patent, copyright, trademark Interest received dividend received Rent received Less : Purchase of fixed assets Purchase of non current investment Purchase of intangible assets such as goodwill, patent copyright, trademark (P.Y. -C.Y.) Capital gain tax paid on sale of fixed asset or non current investment Adjust Extraordinary items (+/–) (eg. Add insurance claim on fixed asset lost due to fire or natural calamities) | |||

| II. Cash flow from (or used in) Investing activities | |||

| Cash flows from financing activities Add : Proceeds from issue of equity shares, preference Shares and debentures Proceeds from other long term borrowings, Bank overdraft and short term loans and advances Less : Final dividend/ Interim dividend paid (given in additional information) Proposed dividend (P.Y.) – dividend payable Interest on debentures and loans paid Repayment of loans and advances, Bank overdraft Redemption of debentures, preference shares Premium paid on redemption of debentures and preference shares paid Payment of equity Share, Preference share, debenture issue expenses Dividend distribution tax paid Adjust extraordinary items (+/–) (eg. payment of buyback of share will be subtracted) | |||

| III. Net cash from (or used in) financing activities | |||

| Net increase/Decrease in cash and cash equivalent (I + II +III) Add : cash and cash equivalents in the beginning of the year cash in hand cash at bank short term deposit Marketable securities Current Investment Cheque and Drafts in hand | |||

| cash and cash equivalents in the end of the year Add : Cash in hand Cash at Bank Short term deposits Marketable securities Current Investment Cheque and Drafts in hand |

Following are some of the major items which are not accounted in CFS because it does not involve inflow or outflow of Cash:

- Issue of Equity Shares, Preference Shares or debentures other than cash.

Example – Issue of shares to promoters, issue of shares to creditors to pay off its liability, purchase of fixed asset by issuing shares or debentures to vendors, issue of bonus shares etc.

- Inflow and outflow between components of cash and cash equivalent.

Example – Cash withdrawn from bank for business use, cash deposited into bank, cash realized from cheque deposited into bank, purchase or sale of marketable securities/ current investment etc.

Adjustment entries related to Cash Flow Statement:

- Add back to net profit in operating Activity (P.Y. value)

- Subtract in financing activity ( Proposed dividend (P.Y. value) – Dividend Payable)

2. Interim Dividend / final dividend paid

- Add to net profit in operating activity

- Subtract in financing activity

3. Provision for Income Tax

(This rule will not apply if additional information regarding provision for tax made or income tax paid is given as additional information in the question.)

- Add to net profit in operating activity (C.Y. value)

- Subtract cash generated from operations in operating activity (P.Y. value)

4. When additional information regarding Provision for tax made or income tax paid is given in the question, we prepare provision for tax A/C.

Always remember any of the two will be given in the question either provision for tax made during the year or income tax paid during the year. For instance provision for income tax made is given as additional information then income tax paid will become balancing figure and vice versa. Accounting treatment will change here.

Provision for income tax made during the year will be added to net profit in operating activity.

Income tax paid will be subtracted from cash generated from operations in operating activity. Rule given in adjustment entry 3 will not apply.

5. Preparation of Fixed Asset A/C on original cost basis or when provision for depreciation A/C or accumulated Depreciation A/C is maintained:

In this case, we prepare fixed asset A/C and Provision for Depreciation A/C.

Adjustments related to various items of above two accounts prepared are:

- Gain on sale of fixed Asset – Subtract in operating activity

- Loss on sale of fixed Asset – Add to operating Activity

- Purchase of fixed Asset – Subtract in Investing Activity

- Sale of fixed asset – Add to investing Activity

- Depreciation – Add to operating Activity

*There can be either gain or loss on sale of fixed asset. Both items cannot come together.

6. Preparation of Fixed Asset A/C on written down value Basis that is when provision for depreciation A/C is not maintained:

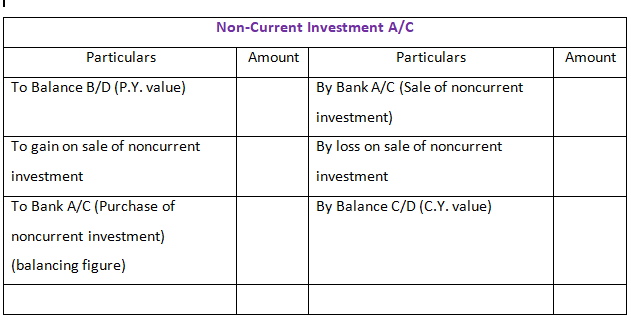

In this case, only fixed Asset A/c is prepared. Noncurrent Investment A/C and Intangible asset A/C are similar to Fixed Asset A/C prepared below. The only difference is that in Non current investment A/c, there will be no depreciation A/C.

Adjustments related to various items of above account prepared are:

- Gain on sale of fixed Asset – Subtract in operating activity

- Loss on sale of fixed Asset – Add to operating Activity

- Purchase of fixed Asset – Subtract in Investing Activity

- Sale of fixed asset – Add to investing Activity

- Depreciation – Add to operating Activity

*There can be either gain or loss on sale of fixed asset. Both items cannot come together.

** Either Purchase of fixed asset/ intangible asset or depreciation/amortization will be balancing figure as per the information given in the question.

3 Comments

AS- 3 Cash Flow Statement, Cash Flow from Operating, Financing & Investing Activity-class-12-accounts-notes – RBL Academy · January 17, 2023 at 7:53 pm

[…] AS- 3 Cash Flow Statement […]

RBL Academy – The Best Choice for Accounts and Economics Coaching in Noida – RBL Academy · March 21, 2023 at 8:57 pm

[…] of experience and a team of highly qualified teachers, RBL Academy has been providing quality coaching to students for […]

Benefits of Hiring a Home Tutor for Class 11 and 12 Accounts and Economics – RBL Academy · March 28, 2023 at 9:51 pm

[…] If you are a student in class 11 or 12 and studying accounts and economics, you may have considered hiring a home tutor. Home tuition can be a great way to supplement your classroom learning and ensure that you are able to understand and apply the concepts effectively. In this blog, we will discuss the benefits of hiring a home tutor for class 11 and 12 accounts and economics. […]